04

Nov

2016

Tax Implications of a President Clinton or a President Trump

By Nicholas Wesley Yee, CPA

By Nicholas Wesley Yee, CPA

Director of Research at Gradient Analytics

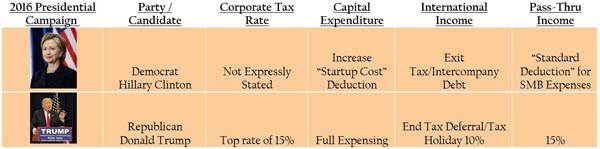

With the 2016 U.S. Presidential Elections coming into the final stretch, Gradient Analytics (a forensic accounting research firm, and a wholly-owned subsidiary of Sabrient Systems) recently published a tax issue commentary for its institutional clients. Included was discussion of the possible impact of each of the two major candidates on the tax code.

The U.S. Tax Code has evolved, in part, as a mechanism to shape economic and political agendas. Similar to the “code” in a computer program, over the years the U.S. Tax Code has experienced numerous modifications, additions, and pet projects of politicians that were built upon the existing code. And similar to a computer program, the continuous accretion of line items to the original code can cause issues that reverberate throughout the entire program. There comes a time when it is more beneficial to scrap the old code and start from scratch so that the entire program can be built harmoniously in nature. While easy enough for a programmer to achieve, the political obstacles that would have to be dealt with in a complete tax code rewrite would likely prove to be too much to overcome. Which leads us to the current presidential candidates and their thoughts on the situation.

;

;