by Scott Martindale

CEO, Sabrient Systems LLC

Quick note: The previous website had some issues, but I invite you now to visit https://MoonRocksToPowerStocks.com to learn more about Sabrient founder David Brown’s new book, Moon Rocks to Power Stocks, which teaches how to build wealth through data and discipline. You can immediately download the book and two bonus reports (on investing in the future of Energy and Space Exploration) in PDF format and learn how to access the Sabrient Scorecards subscription product.

Overview

War and its impact on oil, LNG, and fertilizer supplies and pricing—and by extension the impact on inflation, supply chains, bond yields and mortgage rates, dollar strength, global liquidity and global GDP—continue to top the headlines. And as if that’s not enough, we have our worsening political polarization, an utterly feckless US Congress, and complete lack of bipartisan agreement on anything, with the severe fallout of no DHS funding and long TSA lines at the airport. And lest we forget, we have rising debt and expanding deficits, sticky services inflation, and a softening labor market with falling job openings, layoffs, stalled wage growth, and new college graduates facing rising unemployment. But the buildout of physical AI infrastructure is creating real ROI, wealth creation, and productivity gains, and the companies building the AI compute stack have been delivering incredibly bullish earnings calls and forward guidance—and they are not dissuaded in the least by any of those onerous macro issues.

The doomsayers have been joined by the realists and pragmatists in believing there is no escaping $150/bbl oil and an economic recession, depending upon how much longer the oil market and energy supply chain disruption goes on—leaving only the eternal optimists to carry the bullish flag. History shows that stocks tend to recover nicely following military conflicts that are resolved relatively quickly, finding a bottom concurrently with the peak in oil prices. But production and refining capacity take to time to bring back online, and destruction of energy infrastructure among the Gulf Cooperation Council countries (GCC—Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and UAE) can take years to rebuild. If the Iranian regime tries to take it all down concurrent with their own demise, including crippling their own Kharg Island facilities—the future of their own citizens be damned—then the near-term future indeed may be challenging (or even bleak).

The war continues to consume precious resources and disrupt the global economy, as the whole world waits out with bated breath each missile launch and utterance from our president. President Trump’s goals are to defang Iran’s military and long-range missile capability, nuclear infrastructure, and terrorist network, and decapitate its radical, hateful, theocratic regime (and hopefully usher in a friendlier government) without destroying the civilian infrastructure and power grid so that the Iranian people (and the country’s future) aren’t catastrophically crippled. Indeed, rather than Trump “TACOing” again on harsh escalation (i.e., chickening out, as his critics accuse him of), I believe it is really an indication of his desire not to cripple Iran’s future as a thriving participant in the global economy. Trump doesn’t require a secular democracy there; he just wants to see a responsible, approachable government that doesn’t oppress its people, threaten all non-believers with death, aspire to a global caliphate, or zealously pursue an apocalyptic ending that ushers in the “Twelfth Imam.”

What’s left of Iran’s tyrannical regime is behaving like the Black Knight in the old comedy movie, Monty Python and the Holy Grail. Although thoroughly defeated, the regime just keeps on with its impotent saber-rattling. “It’s just a flesh wound!” the Black Knight exclaims after King Arthur chops off his arm. And after the king has chopped off all his arms and legs, the Black Knight says, “Alright, we’ll call it a draw.” Here’s the 4-minute clip. I have much more to say about the Iran War in my Final Comments section below.

Unfortunately, enough market participants are worried that maybe the Iranian regime’s bluster has a kernel of truth, or that US boots on the ground will lead to intolerable death and destruction in a bloody effort to take control of Kharg Island and ship traffic in the Strait of Hormuz. My view is that the regime is flailing like the Black Knight, and that the end is near. No money, dwindling munitions and resources. JP Morgan CEO Jamie Dimon opined that he is optimistic about the aftermath of the war given the new mentality across the region born of recent strong economic growth that has been creating incentives for stability and a desire among the GCC for a “permanent peace in the Middle East” that would open the region to foreign investment and robust growth. He said, “The Iran war gives it a better chance in the long run; [but] it’s probably riskier in the short run." BlackRock’s Larry Fink sees just two extreme potential outcomes with no middle ground: either we see growth, abundance, and $40 oil, or we see global recession and years of $150 oil. It’s worth noting that spikes in oil-to-natural gas ratio historically have receded within a few months; however, destroyed energy infrastructure could easily change this dynamic.

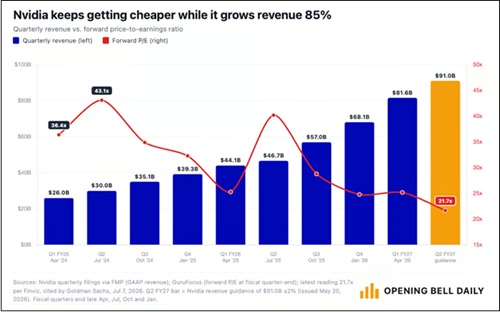

Since its all-time high of 7,000 on 1/28, the S&P 500 is down about 9% (as of 3/30), which means it has lost over $5 trillion in market cap, mostly due to fear-driven selling but also profit protection, capital preservation, and algo trading that is now short-biased. On Friday 3/27 alone, the MAG-7 stocks shed $330 billion in market cap. Traders have been clearing out positions ahead of each weekend due to uncertainty about war escalations. Even holding overnight is worrying for them. The Dow and Nasdaq have fallen more than 10% (i.e., correction territory). Investor trepidation has led to beat-and-raise earnings reports from dominant Tech companies being met with selling—notably Micron (MU) and its incredible quarterly report that confirmed huge demand for AI memory, as well as NVIDIA (NVDA) and its 73% YoY revenue increase that defied the “law of large numbers” for the largest market cap company in the world. Despite seeing its market cap contract for over $5 trillion to closer to $4 trillion, NVIDIA remains an incredibly profitable company with remarkable margins and ROE, and an index weighting of about 8% of the S&P 500—which is more than the weightings of 5 of the 11 GICS sectors (Consumer Staples, Energy, Utilities, Materials, and Real Estate).

The forward P/E on the S&P 500 has fallen from a high around 23x to around 20x today, which is near its 10-year average, The CBOE Volatility Index (VIX) closed last week in panic territory above 31. Bonds have offered no safe haven as auctions have seen limited demand. Nor have gold, silver, and crypto as the US dollar has firmed up and central banks, which had been accumulating gold in a big way, find they desperately need to sell non-interest-bearing assets (like gold) to raise money to either offset lost oil export revenue or to pay the surging price of oil imports. But money is flowing into hard assets, like oil, agriculture, industrial metals, and commodities broadly. Some say the dominos are stacking up much like 2008, this time driven by surging oil prices and a potential meltdown in private credit. The chart below shows the divergent performance of various asset class ETFs, including oil (USO), commodities (DBC), driven mostly by oil and gasoline prices which have seen their biggest surge in four years, agriculture (DBA), bitcoin (BTC-USD), long-term US Treasuries (TLT), and gold (GLD).

This market correction has served to reset lofty valuations in prominent names that many investors want to own for the long term. Keep in mind, large capital spending commitments for AI, defense, and energy projects persist and even grow, such as Meta Platforms’ (META) announcement of an increase in its investment in a state-of-the-art, 1.0 GW AI datacenter in El Paso, Texas, raising its projected capex for the project from $1.5 billion to over $10 billion, as part of a total $135 billion capital spending plan for 2026, creating 4,000 construction jobs and ultimately 300 permanent operations jobs. Moreover, it will be water-positive by employing a closed-loop cooling system, and the company will fully fund all associated infrastructure and power grid connections. This is why engineering & construction firms like Comfort Systems (FIX)—the top performer in our next-to-terminate Q1 2025 Baker’s Dozen—and Sterling Infrastructure (STRL)—a top performer in our Q2 2025 and Q3 2025 Baker’s Dozens—have held up so well despite the profit-taking in their benefactors. I talk more about these firms in my full commentary.

The One Big Beautifull Bill Act (OBBA) has fully kicked in, with its tax reform, deregulation, pro-energy policies, and broad support for the private sector to retake its rightful place as the primary engine of growth via re-privatization, reshoring, and re-industrialization, with much more efficient capital allocation and ROI than government. US corporate earnings are expected to increase by 17% YoY in full-year 2026, according to FactSet—the most since the post-pandemic recovery and a level more typical of an economy emerging from a recession—as analysts keep revising upwards even as share prices fall. However, as DataTrek pointed out, while earnings growth isn’t a concern, Big Tech reinvestment rates are a concern (i.e., capex/cash flow ratio). To be sure, analyst optimism on earnings assumes only a temporary war shock and continued tech strength. As Barclays sees it, “There is a wall of worry—but it’s worth climbing.”

Yes, the Iran hostilities have created vast uncertainties and impacts on energy and supply chains—and by extension inflation. But I still think the overall picture suggests room for another Fed rate cut (certainly not a rate hike!). I go further into all of this in my full post below, including the economy, inflation, Fed policy, and the continued promise of the Tech sector. Then I close with my Final Comments section to expand on my opinions on the Iran “excursion” and the politics around it here at home, followed by an update on Sabrient’s sector rankings, positioning of our sector rotation model, and some top-ranked ETF ideas.

Looking ahead, stock market performance should be more dependent upon earnings growth and ROI rather than multiple expansion—although with this market correction, valuations have pulled back to the 10-year average, which may leave room for some multiple expansion as well. But regardless, rather than the broad passive indexes (which are dominated by growth stocks, Big Tech, and the AI hyperscalers), I think 2026 should continue to be a good year for active stock selection, small caps, and bond-alternative dividend payers—which bodes well for Sabrient’s Baker’s Dozen, Forward Looking Value, Small Cap Growth, and Dividend portfolios, which are packaged and distributed as unit investment trusts (UITs) by First Trust Portfolios.

Witness our Baker’s Dozen portfolios, which have held up relatively well compared to the benchmark S&P 500. The Q1 2026 portfolio (launched 1/17/26) is down only -1.7% vs. -6.1% for SPY (as of 3/27/26). It is led by refiner Valero Energy (VLO) and digital storage maker Western Digital (WDC). It remains in primary market until the Q2 2026 Baker’s Dozen launches on 4/17/26. Notably, last year’s Q1 2025 Baker’s Dozen that terminates on 4/16 has more than tripled the benchmark with a gross total return of +26.3% vs. +7.8% for SPY (as of 3/27/26).

Also, small caps and high-dividend payers tend to benefit from falling interest rates and market rotation—which should resume as the war comes to a (hopefully swift) resolution. Roughly 2/3 of Russell 2000 companies topped Q4 earnings expectations, which is the best beat rate since 2021 (coming out of the pandemic). So, Sabrient’s quarterly Small Cap Growth and Dividend portfolios might be timely investments. And, as a reminder, our Earnings Quality Rank (EQR) is licensed to the actively managed, low-beta First Trust Long-Short ETF (FTLS) as a quality prescreen. Worth checking out.

I have been imploring investors in my recent posts to exploit any significant market pullback by accumulating high-quality stocks as they rebound, with earnings fueled by massive capex in AI, blockchain, energy, and onshoring of power infrastructure and factories, leading to rising productivity, increased productive capacity, and economic expansion. By “high-quality stocks,” I mean fundamentally strong, displaying a history of consistent, reliable, resilient, durable, and accelerating sales and earnings growth, positive revisions to Wall Street analysts’ consensus estimates, a history of meeting/beating estimates, rising profit margins and free cash flow, high capital efficiency (e.g., ROI), solid earnings quality and conservative accounting practices, a strong balance sheet, low debt burden, competitive advantage, a wide moat, and a reasonable valuation compared to its peers and its own history.

These are the factors Sabrient employs in our quantitative models and portfolio selection process. As former engineers, we use the scientific method and hypothesis-testing to build models that make sense. As a reminder, Sabrient founder David Brown reveals the primary financial factors used in our models and his portfolio construction process in his latest book, Moon Rocks to Power Stocks—now an Amazon international bestseller.

Here is a link to this post in printable PDF format, where you also can find my latest Baker’s Dozen presentation slide deck. As always, I’d love to hear from you! Please feel free to email me your thoughts on this article or if you’d like me to speak on any of these topics at your event! Read on….

by Scott Martindale

by Scott Martindale As most everyone expected, Congressional brinksmanship gave way to an eleventh hour agreement that will put the government back in business and raise the debt ceiling. However, it’s only a temporary measure that merely defers another knock-down/drag-out for a few months. The question is, how will investors react after an initial bullish burst of relief?

As most everyone expected, Congressional brinksmanship gave way to an eleventh hour agreement that will put the government back in business and raise the debt ceiling. However, it’s only a temporary measure that merely defers another knock-down/drag-out for a few months. The question is, how will investors react after an initial bullish burst of relief? That’s been hard to figure lately. Uncertainty has not eased. Not in Europe. Not in the Middle East. Not in China or Japan. Not in the U.S., with a dead-heat election battle and unknown future Congressional dynamics. Companies overall continue to beat earnings, mostly, and miss on revenues. Now there is a certainty: earnings cannot keep going up if revenues keep going down.

That’s been hard to figure lately. Uncertainty has not eased. Not in Europe. Not in the Middle East. Not in China or Japan. Not in the U.S., with a dead-heat election battle and unknown future Congressional dynamics. Companies overall continue to beat earnings, mostly, and miss on revenues. Now there is a certainty: earnings cannot keep going up if revenues keep going down. Five years ago this month, the S&P 500 hit all-time high of 1576. It closed Wednesday at 1461. Can the market make a run at that all-time high? Well, the biggest threat at the moment to bullish sentiment is the Fiscal Cliff, but both presidential candidates have a plan for dealing with it, and Congress is unlikely to want to take the fall for defying the new President and sending the country back into recession.

Five years ago this month, the S&P 500 hit all-time high of 1576. It closed Wednesday at 1461. Can the market make a run at that all-time high? Well, the biggest threat at the moment to bullish sentiment is the Fiscal Cliff, but both presidential candidates have a plan for dealing with it, and Congress is unlikely to want to take the fall for defying the new President and sending the country back into recession.